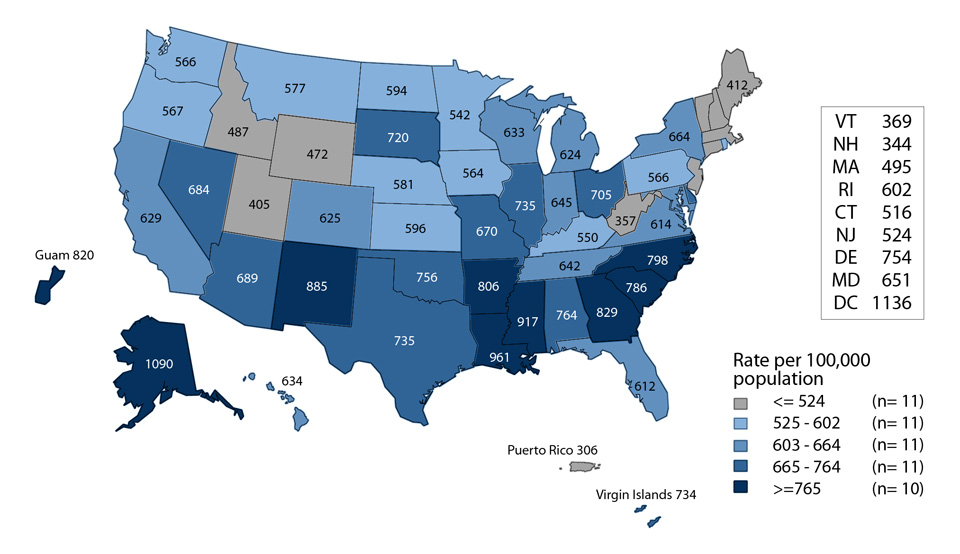

Puerto rico department of state: Government of Puerto Rico | USAGov

Home

Heading

Heading

Heading

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Button Text

Text Link

Heading

Heading

Heading

Heading

Heading

Heading

Heading

Heading

Heading

Heading

Registry of

Corporations and Entities

The Department of State is responsible for administering the public registry of legal entities in Puerto Rico or authorized to do business in Puerto Rico, whether for profit or not-for-profit.

Go to page

Passport

Services

Passport offices process Passport and Passport Card applications for U.S. citizens living in Puerto Rico.

Go to page

Information for

Entrepreneurs

The Department of State supports entrepreneurs through corporate, trademark and trade name registrations and business transactions.

Go to page

Executive Orders

Executive Orders are an instrument of the Governor derived from the exercise of executive power by force of law, whereby the Governor issues an order to an Executive Branch entity.

Go to page

Proclamations

Proclamations seek to educate on issues that can benefit the community in some social aspects.

Go to page

Bylaws

The Electronic Registry allows searches of Agency Bylaws registered with the Department of State.

Go to page

Recent News

State Department processes 11,000 more passports than last year

The Passport Office of the Puerto Rico Department of State (PRD) handled 11,391 additional passport applications compared to the same date last year, Secretary of State Omar J. Marrero Díaz announced today.

See more

Governor Pierluisi joins mourning for the death of the Queen of England

September 8, 2022- The governor of Puerto Rico, Pedro R. Pierluisi, joined the mourning after the death of the Queen of England, Elizabeth II, and instructed that the flags remain at half-mast in all government agencies….

See more

Secretary of State receives J-1 Visa Exchange Visitor Program students and professors

September 8, 2022 [San Juan, Puerto Rico] Secretary of State Omar J. Marrero Díaz received 14 students and professors participating in the J-1 Visa Exchange Visitor Program. This program is attached to the Office of…

See more

Lorem ipsum

Secondary Information

Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit.Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit.Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit.

CTA/LINK

Lorem ipsum

Secondary Information

Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit. Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit.Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit.

Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit.Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit.

CTA/LINK

Lorem ipsum

Secondary Information

Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit.Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit.Card description Lorem ipsum dolorsit amet, consectetuer adipiscing elit.

CTA/LINK

Services

As one of the most important governmental instrumentalities, the Department of State is responsible for fostering cultural, political and economic relations between Puerto Rico and foreign countries as well as with other jurisdictions of the United States of America. In addition, it performs various administrative functions such as:

- To enact, publish, certify, and sell the laws and bylaws of the Government of Puerto Rico;

- To regulate the use of the flag and coat of arms of Puerto Rico;

- To issue licenses for the exercise of professions or trades regulated by the State through the Examining Boards;

- Preparing and keeping various registries: consuls; corporations and partnerships; trademarks; notaries and intellectual property, among others.

- Process passport applications for U.S. citizens, a task delegated by the Federal Government;

- Coordinate matters of a protocol nature that fall within the Government’s purview.

The Department of State offers several services for citizens, businesses and foreigners, among them:

PassportsTrademark RegistrationsCorporationsImmigration Services

Popular forms

For your convenience, we have collected here some of the most searched forms by citizens on our platform. Download them and fill them out in advance to speed up your dealings with the Department of State.

Press credentials application

Legal entity registration forms

Basic incorporation

guide

DS-11 first time passport

application

DS-82 application for passport renewal

DS-3053 consent form for minors under 16

Administrative

Documents

Administrative documents are available on the Department of State’s website so that our citizens always have the most relevant information at hand.

Go to page

Puerto Rico – The Legal 500

Overview of Puerto Rico

- Currency: United States dollar

- Dimensions: 100 x 35 miles (160 by 56 kilometers)

- Climate: Tropical, 82 degrees Fahrenheit (28° C) annual average temperature

- Time Zone: “Atlantic Standard Time”. For most of the year, due to “Daylight Savings Time”, March through November has the same time as the East Coast of the United states.

- U.S. Jurisdiction: Puerto Rico is a United States territory and, thus, offers businesses the security and stability to operate in a U.S. jurisdiction. Moreover, no passport is required for United States citizens when traveling from the mainland to and from Puerto Rico. Our main airport is easily accessible from most hubs (New York, Miami, Texas, Panama City and Madrid) and travel within the Island is extremely accessible and fast.

- Legal system: Puerto Rico enjoys United States constitutional, legal, financial and regulatory protection, including for intellectual property and Homeland Security matters. Its banking system is regulated under the United States laws and insured by the Federal Deposit Insurance Company (FDIC) and our access points are protected by the U.S. Customs and Border Patrol. Puerto Rico enjoys the benefits of being a United States free trade zone and our citizens and residents enjoy federal grants and funds available to the United States citizens located in the mainland. It also shares common military defense with the U.S.

- Geographical advantage: Puerto Rico is located in the eastern Caribbean and is the smallest of the Greater Antilles. Its geographical location strategically positions Puerto Rico between North America and South America and makes it the link between the United States and the Latin America markets.

- Workforce: Puerto Rico offers a skilled, highly educated, and talented bilingual workforce. The Island enjoys a wide cultural diversity founded in the different backgrounds of people that have converged in the Island throughout its history. Many of our residents, who are United States citizens, are fully bilingual (official languages are Spanish and English). Puerto Rico has highly educated human capital; more than 30,000 university degrees are granted annually, including 10,000 in the science, mathematics and technology areas. Therefore, most of its workforce is highly educated and focused on providing a high standard of quality and services.

- Local tax system: The local tax system is regulated by the Department of the Treasury of Puerto Rico. Because Puerto Rico is a United States territory, corporations are not subject to federal taxes unless earnings are repatriated. In turn, the corporate tax structure provides benefits of operating at a United States jurisdiction while providing tax benefits of a foreign country. Puerto Rico has also developed laws providing incentives and tax exemption benefits for multiple industries and activities, including manufacturing, research and development, export services, tourism and film, among others. Legislation also provides attractive benefits to individual investors that become Puerto Rico residents.

Its banking system is regulated under the United States laws and insured by the Federal Deposit Insurance Company (FDIC) and our access points are protected by the U.S. Customs and Border Patrol. Puerto Rico enjoys the benefits of being a United States free trade zone and our citizens and residents enjoy federal grants and funds available to the United States citizens located in the mainland. It also shares common military defense with the U.S.

Its banking system is regulated under the United States laws and insured by the Federal Deposit Insurance Company (FDIC) and our access points are protected by the U.S. Customs and Border Patrol. Puerto Rico enjoys the benefits of being a United States free trade zone and our citizens and residents enjoy federal grants and funds available to the United States citizens located in the mainland. It also shares common military defense with the U.S. Many of our residents, who are United States citizens, are fully bilingual (official languages are Spanish and English). Puerto Rico has highly educated human capital; more than 30,000 university degrees are granted annually, including 10,000 in the science, mathematics and technology areas. Therefore, most of its workforce is highly educated and focused on providing a high standard of quality and services.

Many of our residents, who are United States citizens, are fully bilingual (official languages are Spanish and English). Puerto Rico has highly educated human capital; more than 30,000 university degrees are granted annually, including 10,000 in the science, mathematics and technology areas. Therefore, most of its workforce is highly educated and focused on providing a high standard of quality and services. Legislation also provides attractive benefits to individual investors that become Puerto Rico residents.

Legislation also provides attractive benefits to individual investors that become Puerto Rico residents.Doing business in Puerto Rico

Incorporation of Registration to do Business in Puerto Rico

Businesses establishing operations in Puerto Rico usually organize as a Corporation or a Limited Liability Company (“LLC”) under the laws of Puerto Rico. In Puerto Rico, any natural or corporate person may organize a corporation or LLC. The entities are created by filing the Articles of Incorporation (corporations) or Articles of Organization (LLC’s) with the Puerto Rico State Department, where they become available for public inspection, and by paying an incorporation fee based on the authorized capital stock of the corporation. In most cases, the articles may be electronically filed using the Department of State’s website at https://estado.gobierno.pr. Newly incorporated or organized entities must apply for and obtain an Employer Identification Number (“EIN”) with the United States Internal Revenue Service (“IRS”).

Alternatively, businesses organized under the laws of a state of the United States or a foreign country may register to be authorized to conduct business within Puerto Rico as a foreign corporation. These businesses must file with the Puerto Rico State Department a “Certificate of Authorization to do Business”. The application must set forth its name, place and date of incorporation, physical address of its corporate domicile, address of its registered office and name of its resident agent in Puerto Rico, names and business address of its directors and officers, a statement of its assets and liabilities, a description of the business it proposes to carry on in Puerto Rico, and a statement that it is authorized to do business in the jurisdiction of its incorporation.

LLC Classification Election

The default classification for Puerto Rico LLCs under the Federal Internal Revenue Code is to be taxed as an “association taxable as a corporation”. Puerto Rico LLCs that desire to be taxed as a flow through entity (either as a Partnership or as a Disregarded Entity) under the Federal Internal Revenue Code must file an election to that effect (the “Federal Classification Election”) with the United States Internal Revenue Service. The Federal Classification Election must be filed using Form 8832 and may be provide for an effective date of up to 75 days prior to the actual filing date.

The Federal Classification Election must be filed using Form 8832 and may be provide for an effective date of up to 75 days prior to the actual filing date.

All (i) PR LLCs (regardless of their classification under the Federal Internal Revenue Code) and (ii) Non-PR LLCs that for Federal tax purposes are taxed as an “association taxable as a corporation” may elect to be taxed as either a corporation or a partnership for purposes of the Puerto Rico Internal Revenue Code. These LLCs must file a classification election (the “PR Classification Election”) with the Puerto Rico Department of Treasury (“PRTD”).

Non-PR LLCs that for Federal Tax Purposes are taxed as either “Partnerships” or “Disregarded Entities” will be taxed as partnerships for purposes of the Puerto Rico Internal Revenue Code. These LLCs must file a notice of their Puerto Rico tax classification as a “partnership” with PRTD.

Puerto Rico Treasury Registration

The Puerto Rico taxpayer account number will be the same as the federal EIN. Upon receipt of the EIN from the IRS, and prior to commencing operations, companies must inform the EIN to the PRTD by registering in the Uniform System of Internal Revenue (“SURI” for its Spanish acronym). The taxpayer must provide copy of the letter from the IRS assigning the EIN. To access SURI, the business must visit the PRTD’s website https://suri.hacienda.pr.gov. To register in SURI, the business must provide an email address and create a user account.

Upon receipt of the EIN from the IRS, and prior to commencing operations, companies must inform the EIN to the PRTD by registering in the Uniform System of Internal Revenue (“SURI” for its Spanish acronym). The taxpayer must provide copy of the letter from the IRS assigning the EIN. To access SURI, the business must visit the PRTD’s website https://suri.hacienda.pr.gov. To register in SURI, the business must provide an email address and create a user account.

Merchant Sales and Use Tax Registration

Generally, all sales (or the use, consumption, or warehousing) of a taxable item or a taxable service in Puerto Rico are subject to a 11.5% sales and use tax (IVU for its Spanish acronym) that includes a 10.5% state sales and use tax, and a 1.0% municipal sales and use tax. In the case of services rendered to other merchants or designated professional services, the sales and use tax rate is 4%.

To comply with the Puerto Rico sales tax provisions and be authorized to collect the sales tax from their customers, all merchants are required to register in SURI. Once a company registers, it will electronically receive, through SURI, a Merchant’s Registration Certificate (Form SC 2918) which must be placed in a location of the business that is visible to the general public. If the company is engaged in a business that is exempted from the collection of sales taxes, it must still register. The exempted company will receive Merchant’s Registration Certificate indicating that it is exempt from collecting the sales tax. Each location from which the business will be conducting its operations will require a separate Merchant’s Registration Certificate.

Once a company registers, it will electronically receive, through SURI, a Merchant’s Registration Certificate (Form SC 2918) which must be placed in a location of the business that is visible to the general public. If the company is engaged in a business that is exempted from the collection of sales taxes, it must still register. The exempted company will receive Merchant’s Registration Certificate indicating that it is exempt from collecting the sales tax. Each location from which the business will be conducting its operations will require a separate Merchant’s Registration Certificate.

Municipal Business License

Companies must apply for a municipal business license within 30 days of commencing operations in the municipality(ies) where it will conduct business. The notification must include a copy of the certificate of incorporation or authorization to do business in Puerto Rico, a copy of the lease agreement, and a copy of the “Use Permit” for the facility to be used within the Municipality.

Upon receipt of the notice of commencement of operations, the Director of Finance of each municipality will issue a provisional certificate or license free of tax for the semester corresponding to that in which such activity commenced. For the next semester, a business volume declaration, together with the corresponding tax must be filed with and paid to the municipality within the first 15 days of the semester. The business volume will be the one derived during the first semester of operations raised to an annual basis.

Local Labor Law Requirements for Private Companies

Social Security and Medicare Withholdings – per federal law, employers must generally withhold part of social security and Medicare taxes from employees’ wages and employees pay a matching amount.

- Vacation Days – Non-exempt employees accrue vacation leave in every month they work at least 130 hours. In Puerto Rico, exempt employees are not entitled to statutory vacation leave. However, many employers in Puerto Rico consistently offer either the statutory, or some form of vacation leave to exempt employees, as part of the benefits to such employees. Non-exempt employees are entitled by law to the liquidation of the accrued but unused balance of vacation leave at the time of termination.

- Sickness Days – Non-exempt employees accrue paid sick leave in every month they work at least 130. Payment for sick leave will be based on the regular workday at the time the benefit is used or paid. Sick leave is not paid upon termination of employment. In Puerto Rico, exempt employees are not entitled to statutory sick leave. However, many employers in Puerto Rico consistently offer the statutory, or some form of sick leave, to exempt employees as part of the benefits to such employees.

- Christmas Bonus – Employees who have worked at least 1350 hours (or 700 hours if hired prior to January 26, 2017) within the twelve (12) month period between October 1 of the previous calendar year and September 30 of the current calendar year, will be eligible to receive an Annual Christmas Bonus. The amount of the Annual Christmas Bonus will depend on the employee’s date of hire and the size of the employer’s workforce. Employees hired on or after January 26, 2017, may be entitled to an Annual Christmas Bonus of at least two percent (2%) of their annual salary (up to a maximum of $300.00 or $600.00, depending on the number of employees).

- State Insurance Fund – The cost of the premium payable by employers to the State Insurance Fund Corporation for workers’ compensation due to occupational accidents or illnesses depends on the salary of the employees and their employment classification under the State Insurance Fund’s risk classifications. Employees on leave due to a work-related accident covered by the State Insurance Fund have a 12-month (6 months in case of employers with 15 employees or less) reserve of employment from the day of the occupational accident or injury occurred, under certain circumstances.

- Chauffeur’s Social Security Insurance – Employers are only obligated to pay premiums for this government-mandated insurance for non-exempt employees who, as part of their duties and responsibilities, regularly operate a motor vehicle (including fork-lifts). The premiums are .80 cents per week per non-exempt employee. The employer may deduct .50 cents from the employee’s weekly payroll and the company will contribute the remaining .30 cents. Reservation of employment applies to employees receiving these benefits.

- Unemployment Insurance – The unemployment policy premium is based on the employer’s experience rating with the Puerto Rico Department of Labor. The percentage of the premium is notified to the employer once it requests its account number with the Puerto Rico Department of Labor.

- SINOT (Short Term Non-Occupational Disability Insurance) – (SINOT) is calculated alongside the mandatory unemployment insurance and is also obtained from the Puerto Rico Department of Labor. The SINOT premium is .60% of employees’ yearly wages without taking into consideration those wages paid in excess of $9,000. (Employer and employee divide the cost at .30% each. Some employers, however, opt to voluntarily pay the totality.) Reservation of employment applies to employees receiving these benefits.

- Termination of Employment – Puerto Rico is not an “employment at will” jurisdiction. Thus, indefinite-term employees discharged without just cause are entitled to receive a statutory severance payment based on the length of their employment and salary, pursuant to the statutory formula.

- Meal period – Non-exempt employees are entitled to a meal (or rest) period of one hour in length, unless the employer and the employee mutually agree in writing to reduce its length if the reduction is for the mutual benefit of the employer and employee.

Non-exempt employees are entitled by law to the liquidation of the accrued but unused balance of vacation leave at the time of termination.

Non-exempt employees are entitled by law to the liquidation of the accrued but unused balance of vacation leave at the time of termination. Employees hired on or after January 26, 2017, may be entitled to an Annual Christmas Bonus of at least two percent (2%) of their annual salary (up to a maximum of $300.00 or $600.00, depending on the number of employees).

Employees hired on or after January 26, 2017, may be entitled to an Annual Christmas Bonus of at least two percent (2%) of their annual salary (up to a maximum of $300.00 or $600.00, depending on the number of employees). The premiums are .80 cents per week per non-exempt employee. The employer may deduct .50 cents from the employee’s weekly payroll and the company will contribute the remaining .30 cents. Reservation of employment applies to employees receiving these benefits.

The premiums are .80 cents per week per non-exempt employee. The employer may deduct .50 cents from the employee’s weekly payroll and the company will contribute the remaining .30 cents. Reservation of employment applies to employees receiving these benefits.

Statutory Filing Requirements of Companies Resulting from the Regular Course of Business after Commencing Operations in Puerto Rico

A. Corporate Income Tax Return

For taxable years commencing after December 31st, 2018, the taxable income of corporations is taxed at a regular tax rate of 18.5% (the “Regular Corporate Tax”). In addition, the taxable income of corporations is also subject to an additional tax at graduated rates that range from 5% to 19% (the “Additional Corporate Tax”).

In addition, dividend distributions made by Puerto Rico Corporations, or by Non-Puerto

Rico Corporations that derive at least 80% of their gross income from sources within Puerto Rico, to their Non-Puerto Rico shareholders, are subject to a 10% withholding tax.

Non-Puerto Rico Corporations that derive less than 80% of their gross income from sources within Puerto Rico are not subject to the withholding tax on dividends. However, they are subject to a 10% Branch Profits Tax (the “BPT”) on any reductions in their Puerto Rico net equity, but only to the extent that the Non-Puerto Rico Corporation has any current or accumulated earnings and profits that were derived from the conduct of a Puerto Rico trade or business (the “Dividend Equivalent Amount”).

The Puerto Rico Corporation Income Tax Return must be filed on or before the 15th day of the 4th month following the close of the taxable year. An automatic 6-months extension to file the income tax return may be requested through SURI. All businesses with a volume of business in excess of $3,000,000.00 must include, with their income tax return, audited financial statements prepared by a Certified Public Accountant licensed to practice in Puerto Rico.

All businesses with a volume of business in excess of $3,000,000.00 must include, with their income tax return, audited financial statements prepared by a Certified Public Accountant licensed to practice in Puerto Rico.

B. Partnership Income Tax Return

As discussed above, under the Puerto Rico Internal Revenue Code, partnerships (including LLCs electing to be taxed as partnerships) are treated as pass-thru entities. Accordingly, the partnership will not be taxed on its taxable income, which will instead flow thru and be taxed to its partners. In that sense, partnerships must file an Informative Income Tax Return for Pass-Through Entity and their income flows thru and is taxed to the partners at the partners’ income tax rate.

Regardless of the above, the partnership is responsible for depositing with the PRTD, an amount equal to 30% of its Taxable Income (the “Tax Deposits”), which will be credited to the tax liability of the partners. All of the partners will be required to file an income tax return with the PRTD. The partners must include, as part of their taxable income, their distributable share of the partnership’s taxable income and will be entitled to a credit for their distributable share of the Tax Deposits.

The partners must include, as part of their taxable income, their distributable share of the partnership’s taxable income and will be entitled to a credit for their distributable share of the Tax Deposits.

The Informative Income Tax Return for Pass-Through Entity (Form 480.20 EC), must be filed on or before the 15th day of the 3rd month following the close of the taxable year. An automatic 6-months extension to file the income tax return may be requested through SURI.

The Partnership must also provide each of its partners with an informative return detailing all the information required by the partner for purposes of completing its income tax return. This informative return (Form 480.6 EC) must be filed on or before the last day of the 3rd month following the close of the taxable year through SURI. An automatic 6-month extension to file this return is granted to partnerships that have extended their Forms 480.20 EC.

C. Sales and Use Tax Returns

As a general rule, businesses must collect 11. 5% sales and use tax (“SUT” or “IVU” for its Spanish acronym) on all of their taxable transactions. The 11.5% SUT includes a 10.5% state sales tax and a 1% municipal sales tax. In the case of certain designated professional services and certain services rendered to other registered merchants, the state SUT rate is 4% and the municipal SUT will not apply.

5% sales and use tax (“SUT” or “IVU” for its Spanish acronym) on all of their taxable transactions. The 11.5% SUT includes a 10.5% state sales tax and a 1% municipal sales tax. In the case of certain designated professional services and certain services rendered to other registered merchants, the state SUT rate is 4% and the municipal SUT will not apply.

Merchants collecting the SUT are required to electronically file a monthly SUT return through SURI, which is due on or before the 20th day of the month following the month the SUT was collected (e.g. all tax collections derived from January sales must be reported and paid no later than the 20th of February), and to electronically remit the SUT to the PRTD.

Merchants importing goods into Puerto Rico are also required to electronically file a monthly return with regards to their introduction of goods into Puerto Rico, which is due on or before the 10th day of the month following their introduction of the property (the “Import Return”). All bill of lading documents related to shipments of goods into Puerto Rico must be submitted electronically to the PRTD, which must then authorize the release of the shipments to the recipient after payment of any SUT that may apply to the shipment. Some merchants are allowed to post a bond guaranteeing the payment of the SUT in exchange for the release of their shipments prior to the payment of the SUT. Furthermore, subject to certain limitations, merchant’s may be allowed to claim a credit on their SUT return for a portion or all of the taxes paid with regards to the Import Return.

All bill of lading documents related to shipments of goods into Puerto Rico must be submitted electronically to the PRTD, which must then authorize the release of the shipments to the recipient after payment of any SUT that may apply to the shipment. Some merchants are allowed to post a bond guaranteeing the payment of the SUT in exchange for the release of their shipments prior to the payment of the SUT. Furthermore, subject to certain limitations, merchant’s may be allowed to claim a credit on their SUT return for a portion or all of the taxes paid with regards to the Import Return.

D. Municipal Sales Taxes

The filing requirements for the reporting and payment of municipal sales taxes will depend on the municipality where the business carries out its operations. The municipal portion of the sales tax (1.0%) must be paid directly to the municipality using a “Monthly Sales Tax Return”. Most municipalities have an online platform where you may prepare and filed the monthly municipal sales tax return.

E. PRTD Informative Returns

The Puerto Rico Internal Revenue Code, as amended, provides for the required filing of certain informative returns depending on payments and withholdings made throughout the year.

F. Municipal License Tax (“Patente”)

Generally, the gross revenues of all businesses operating within Puerto Rico are subject to a municipal license tax. Depending on the municipality, the license tax ranges from .2% to .5% of gross revenues for non-financial businesses and may not exceed 1.5% of revenues for financial businesses.

In that sense, businesses must file a Volume of Business Declaration (“VOB”) with each municipality where they operate. The VOB is due five (5) working days after April 15th of each year. A 5% discount is available if the entire municipal license tax is paid with the timely filing of the return. Otherwise, the municipal license tax is payable in two installments, which are due on the July 15th and the January 15th following the due date for the filing of the VOB. Separate returns must be filed with the Director of Finance of each municipality in which the corporation conducts business.

Separate returns must be filed with the Director of Finance of each municipality in which the corporation conducts business.

If the total gross volume of business (gross income) exceeds $3,000,000, the VOB must be accompanied by financial statements, including a balance sheet, income statement, and cash-flow statement, as of the close of the fiscal year ending on the preceding calendar year, audited by a Certified Public Accountant licensed to practice in Puerto Rico. If the volume of business is less than $3,000,000, audited financial statements are not required, and the return must include a copy of the Puerto Rico income tax return filed with the PRTD which details its gross income and operating expenses, together with a statement to the effect that they are true and exact copies of what was filed with PRTD.

G. Municipal Revenue Collection Center (CRIM)

Personal Property Businesses in Puerto Rico are subject to a personal property tax on certain tangible property located within Puerto Rico. Depending on the municipality, the tax rates currently range from 5.83% to 10.33%. Personal property taxes are self-assessed by each business as of January 1st. The self-assessment is made by filing, with the CRIM, a Personal Property Tax Return (“PPTR”) which must be electronically filed with through the CRIM’s website (https://emueble.crimpr.net/). The PPTR and payment of the taxes are due on the 15th of May each year. A single return is used to pay the total tax due to all the municipalities.

Depending on the municipality, the tax rates currently range from 5.83% to 10.33%. Personal property taxes are self-assessed by each business as of January 1st. The self-assessment is made by filing, with the CRIM, a Personal Property Tax Return (“PPTR”) which must be electronically filed with through the CRIM’s website (https://emueble.crimpr.net/). The PPTR and payment of the taxes are due on the 15th of May each year. A single return is used to pay the total tax due to all the municipalities.

An automatic extension of no more than ninety (90) days is granted for corporations by filing Form AS-I, “Request for Automatic Extension of Time to File Personal Property Tax Return”, on or before May 15. The automatic extension must be filed through CRIM’s website, https://emueble.crimpr.net/.

Taxpayers that are subject to the payment of personal property taxes are required to prepay such taxes in four equal installments that will be due on (i) August 15; (ii) November 15; (iii) February 15; and (iv) May 15 (the “Personal Property Tax Installments”). Taxpayers must compute their estimated tax obligation based on a reasonable estimate of the personal property that will be subject to tax on their personal property tax return.

Taxpayers must compute their estimated tax obligation based on a reasonable estimate of the personal property that will be subject to tax on their personal property tax return.

H. Municipal Revenue Collection Center (CRIM) – Real Property

Local law imposes real property taxes on all real property located within Puerto Rico, unless specifically exempted by law. Real property includes the land and subsoil, plus all structures, objects, machinery or implements attached to a building on a permanent manner. Similar to personal property, real property taxes are assessed as of January 1st of each year and paid in two (2) installments due on January and July of each tax year. The real property tax rates vary by municipality and currently range from 8.03% to 12.33%.

I. Department of State Annual Reports

Every Puerto Rico corporation and every foreign corporation authorized to do business within Puerto Rico must annually file, no later than April 15, an annual report with the Puerto Rico Department of State. This report must be filed electronically in Department of State’s website and must be accompanied by an annual fee of $150.

This report must be filed electronically in Department of State’s website and must be accompanied by an annual fee of $150.

LLC’s are not required to file the Corporate Annual Reports. In lieu of the annual reports, they are required to pay an annual fee of $150 to the Puerto Rico State Department.

A 60-day extension may be requested for complying with the filing of the Corporate Annual Reports. No extension is available for the payment of the LLC annual fee.

Payroll Filing Requirements of Companies Resulting from the Maintenance of Employees within Puerto Rico

A. Employer’s Deposit of Social Security and Medicare Taxes

Employers must electronically deposit through the Electronic Federal Tax Payment System (“EFTPS”) the Social Security and Medicare tax withheld with the United States Treasury. The deposit schedule for a calendar year taxpayer is determined from the total social security taxes reported in a four-quarter “look back period,” which begins July 1 and ends June 30.

If the employer reported $50,000 or less of social security taxes during said look back period, the employer is a monthly schedule depositor and must deposit the taxes by the 15th day of the following month in which payments were made. If the employer reported more than $50,000 of social security taxes during said look back period, it becomes a semiweekly schedule depositor and must deposit the taxes on payments made on Wednesday, Thursday and/or Friday by the following Wednesday; and on payments made on Saturday, Sunday, Monday and/or Tuesday by the following Friday (i.e., within the next three (3) banking days).

If the employer’s quarterly tax liability is less than $2,500, no deposits are required, and it must pay the tax with the quarterly return on Form 941 PR. If the employer’s tax liability is $100,000 or more on any day during a deposit period,2 it must deposit the tax by the next banking day, whether it is a monthly or semiweekly schedule depositor.

B. Employer’s Quarterly Federal Tax Return (Form 941 PR)

Employer’s Quarterly Federal Tax Return (Form 941 PR)

Employers in Puerto Rico must file quarterly returns on Form 941 PR, “Employers Quarterly Federal Tax Return,” if Social Security and Medicare taxes were withheld for the quarter, and must pay any undeposited income, Social Security, and Medicare taxes if total tax liability for the quarter was less than $2,500. The returns are due by the last day of the calendar month following the close of each calendar quarter (i.e., by April 30, July 31, October 31, and January 31) and may be filed electronically at the IRS’s website.

C. Employer’s Annual Federal Unemployment Tax Return (Form 940 PR)

Employers in Puerto Rico must file Form 940 PR, “Employer’s Annual Federal Unemployment Tax Return,” by January 31 of the year following the calendar year in which the unemployment tax was accrued, summarizing the unemployment tax accrued during the preceding calendar year.

D. Wages Withholding Statement (Form 499-R-2/W-2 PR)

The original of Form 499-R-2/W-2 PR, “Withholding Statement,” prepared for each employee from whom Social Security tax (“FICA Tax”) was withheld must be filed by the employer, with the Social Security Administration, together with Form W-3 PR, “Reconciliation Statement,” by the last day of February of the year after the calendar year for which withholding was performed through the Social Security Administration’s website, https://www. ssa.gov/bso/bsowelcome.htm.

ssa.gov/bso/bsowelcome.htm.

E. Deposit Slip of Employer’s Monthly Deposit of Income Tax Withheld (Form 499R-1)

Every corporation that maintains employees in Puerto Rico must file Form 499R-1, “Employer’s Monthly Deposit of Income Tax Withheld”, accompanied with deposit of income tax withheld on wages during the preceding month with any PRTD Collector’s Office or any authorized bank. These forms should be filed through the SURI website, https://suri.hacienda.pr.gov.

F. Employer’s Quarterly Return (Forms 499R-1B and 499R-1C)

The quarterly return (Form 499R-1B, “Employer’s Quarterly Return of Income Tax Withheld”) will include information related to the taxes withheld from salaries paid during the preceding calendar quarter, and must be filed by the last day of the calendar month following the close of each calendar quarter (that is, by April 30, July 31, October 31 and January 31) including payment of any undeposited income taxes withheld from wages. Employers in Puerto Rico must electronically file their quarterly returns through the Department of Treasury’s SURI website, https://suri.hacienda.pr.gov.

Employers in Puerto Rico must electronically file their quarterly returns through the Department of Treasury’s SURI website, https://suri.hacienda.pr.gov.

Recent significant changes in local law

- Puerto Rico Incentives Code (Act 60-2019): The Puerto Rico Incentives Code codifies various tax incentives laws into a single code, including tax incentives formerly granted under Act 20 (export services), Act 22 (relocation of individual investors), and Act 73 (manufacturing, research and development, software development and industrial operations), among others, as an economic development tool. Under the Puerto Rico Incentives Code, various sectors may benefit from tax incentives, including traditional sectors such as manufacturing, tourism and agriculture, as well as aerospace, biosciences, technology, renewable energy, entrepreneurship and export services. In addition, it defines new incentives to support emerging sectors, such as the creative, eSports and entertainment industries.

- Puerto Rico Civil Code (Act 55-2020): The Puerto Rico Civil Code is the systemized set of rules of law that regulate our civil relations, including succession and hereditary rights, estate planning, family law, contractual relationships, obligations and torts, real property rights, among others. Puerto Rico’s Civil Code was approved in 1930 based on the Spanish Civil Code and, despite numerous intents to comprehensively amend it, no significant amendments were made until Act 55-2020. The new Civil Code becomes effective on November 28, 2020.

The information provided herein are for informational purposes only and is not intended nor it should be construed as legal, tax or financial advice.

I am based in Alabama and would like to distribute wholesale cigars in Alabama and other states. I will be getting these cigars from suppliers in the Dominican Republic, Puerto Rico and other states. What are my filing requirements?

Official website of the government of the state of Alabama.

That’s how you’ll know

.gov means it’s official

Government websites often end in .gov or .mil. Please make sure you are on the official government website before sharing sensitive information.

The site is safe

The https:// site guarantees that you are connecting to the official site and that any information you provide is encrypted and transmitted securely.

MyAlabamaTaxes

Services

Services

Business and license

Collections

Registration of a legal entity

Human resources

Income tax

Legal

Vehicles

Property tax

Implementation and use

Tax incentives

Tax policy

.gov means it’s official

Government websites often end in .gov or . mil. Please make sure you are on the official government website before sharing sensitive information.

mil. Please make sure you are on the official government website before sharing sensitive information.

The site is safe

The https:// site guarantees that you are connecting to the official site and that any information you provide is encrypted and transmitted securely.

Categories of frequently asked questions of the -questions -dimensacacacon 2021-1 Man breeding of ALTS FIDUSIARY ABOMICIARY Partnerships – Partnerships, Legal Entities and Piduccanis of S -corporations and proxies for electronic submission – Corporations Corporations and Trushing Directorate of Car and Bid Carriage Carpet -Banking Bank and License Environmental Nation Hazardous Waste Scrap Tire Environmental Fee Solid Waste Disposal Storage Tank Trust Fund Motor Fuel Lubricating Oil Pari Mutual Pool Tax and Horse Gambling Government Fee Mineral Extraction Tax Tobacco Tax Business Privilege Tax Consumer Use TaxCorporate Income Tax taxDealer License Alabama Title Deeds Dealer and Manufacturer Plates Designated Agent License Renewal Licenses Legal Registration PersonsExclusionsFilings and PaymentsFinancial Institution Excise Tax Amended Internal Revenue Service Returns and Audits Consolidated TaxpayersDeductions and CreditsElectronic Payment RequirementsEstimated Tax PaymentsFilling RequirementsPostal Addresses Net Operating Losses (NOLs)Tax RatesGarnishesContractor UseCertificateGeneral – Sales from responsibilityHuman resources Internships Income tax 529Savings Plan Construction Employer Fee Withholding on Sale/Transfer of Real Estate and Associated Tangible Personal Property by Non-Residents Personal Income Tax Federal Refund Credit – TOP Filing Forms Collections and Bankruptcy Overview – Personal Income Tax Have you received my refund? Identity Theft and Tax Fraud Income Tax Questions My Alabama Taxes Payments Refunds W2 Reports Installment Payment IRP-IFTA Sale of Land Legal Evaluation Procedures Liability Insurance General Insurance – Liability Insurance Request for Insurance Review Out-of-State Insurance Non-Compliance V Policy Cancellation and Recovery Fees Limited Liability Trust (Form 41) Limited Liability Entities Partnerships and LLEs – Limited Liability Companies Electronic Filing Requirements – LLE S Corporations – Limited Liability Companies Electronic Filing Requirements – S Corporations and LLEsMake Payment Electronic Funds TransferManufactory HomeCarding ONE PLACE Payments in one place ONE TIME returnedPartnership Fiduciary (Form 41) Partnerships and PFAs S Corporations Electronic Filing Requirements – Partnerships S Corporations Electronic Filing Requirements Personal Property Reimbursement Application Real Estate Registration General – Registration License Plate Renewal Personalized License Plate New License Plate Category Offer Vehicle Registration S Corporation Forms1) Fiduciary Forms S Partnerships & Limited Liability Companies – S Corporations E-Filing Requirements – Partnerships & LLCs CorporationsVehicle Recycling & Vehicle Re-Inspection Alabama Assigned VIN General – Vehicle Inspections Restoration Inspection RecyclingSimplified Sales Use TaxPublic Real Estate For SaleTax Account Partner UpgradeTax Benefits Income Tax Benefits for Businesses Excise Tax Payers for Financial Institutions Entrance Entity Administered Taxes Residential Tax Titles General – Titles Lien Bonds Guarantee Title Applications Request Title Records Unclaimed/Abandoned VehiclesVehicle Appraisal Withholding Tax WRAP

View all Business & Licensing, Tobacco Tax FAQs

I am based in Alabama and would like to distribute wholesale cigars in Alabama and other states.

I will be getting these cigars from suppliers in the Dominican Republic, Puerto Rico and other states. What are my filing requirements?

I will be getting these cigars from suppliers in the Dominican Republic, Puerto Rico and other states. What are my filing requirements?

There is no tax on smoking paper in the state. However, some counties impose a tax on smoking paper. Tax rates range from $0.05 to $0.25 per pack.

Similar FAQs in Business & Licenses, Tobacco Tax

What is the duration of the tax lien?

Once the lien arises, it will continue until the accrued amount is discharged, released or unenforceable at the expiration of time (i.e. 10 years from the date the lien was filed) (Sections 40-1-2 , 40-29-20 and 49-29-21 of the Code).

Is there a limit on the number of stamps that can be ordered online?

No. However, the tax stamp ordering system for cigarettes is not tied to consignment balances. Therefore, state consignment clients should be aware of their available consignment balance and place orders within their bond limit. Otherwise, the stamp order will be modified to reflect the available balance.

Otherwise, the stamp order will be modified to reflect the available balance.

Will confirmations be sent that an order has been received and processed?

The person or persons authorized by you to access the MAT/submit an order for stamps will receive confirmation that the order for stamps has been submitted to the Tobacco Tax Office upon clicking on the “submit” button. Once an order has been completed, the invoice associated with the order will be available in MAT for review and payment, if applicable.

Can multiple orders be future dated to cover a specific time period?

No, the system uses the system date when the order was created. Therefore, future-dated orders are not available. If multiple orders are submitted on the same day before 13:00, they will be processed for shipment on the same day; all relevant invoices will have the same billing and payment dates.

How can we notify you about special shipping methods for ordering stamps?

We use FedEx shipping. There is a field in the order form where you can choose the delivery method: pickup, overnight or 2-day delivery. Please use this feature to let our staff know your preferred shipping method. If your FedEx account number is incorrect, please make the necessary changes.

How can I make corrections before placing an order if the wrong brand type or quantity is selected?

Once the “new item” – brand type and quantity – has been saved in the order, it can be edited by entering the correct quantity. You can also select a new type from the drop down list if you have selected the wrong type.

Money Transfer License Information

Alaska

Alaska Department of Communities, Trade and Economic Development

Alaskan residents only.

If Airbnb Payments, Inc., +1 (844) 234-2500, does not resolve your issue, file a formal complaint with the Alaska Department of Banking and Securities.

You can download the form here:

https://www.commerce.alaska.gov/web/portals/3/pub/DBSGeneralComplaintFormupdated.pdf

File a formal complaint with supporting documents: Division of Banking & Securities, PO Box 110807, Juneau, AK 99811-0807.

For all formal complaints, Alaska residents can contact [email protected] or call 9074652521.

California

California Department of Business Administration

If you have a complaint about any aspect of the money transfer business carried out by

in California

you can contact the California Department of Business Enforcement at a toll-free number,

1-866-275-2677,

by email [email protected] or

Department of Business Oversight

Consumer Services

1515 K Street, Suite 200

Sacramento, CA 95814

Colorado

Colorado Department of Banking

CUSTOMER NOTIFICATION

Entities other than FDIC insured financial institutions engaged in money transfer activities in Colorado, including sale of payment orders, transfer of funds and use of other instruments to pay cash or credit must be licensed by the Colorado Banking Department pursuant to Section 11, Section 110 of the Money Transfer Companies Act (Colorado Revised Laws).

If you have a question or problem WITH THE TRANSACTION (MONEY YOU SENT):

Contact the Money Transfer Company that processed your transaction for assistance. The Banking Department does not have access to this information.

If you are a Colorado resident and have a Complaint against the MONEY TRANSFER COMPANY (THE COMPANY THAT SENT YOUR MONEY):

ALL complaints must be in writing. Complete the complaint form located on the Colorado Banking Department website and mail it and any supporting documents by mail or email to the Banking Department at

Colorado Division of Banking

1560 Broadway, Suite 975

Denver, CO 80202

Email: [email protected]

Website: www.dora.colorado.gov/dob

Section 11-110-120, C.R.S. requires money transfer and order companies to post this notice in a conspicuous, well-lit area that is visible to customers.

Florida

Florida Financial Regulatory Authority

To file complaints directly with the Florida Financial Regulatory Authority, mail to:

Florida Office of Financial Regulation

Division of Finance

200 E. Gaines Street

Gaines Street

Tallahassee, FL 32399-0376

Toll Free: 1-800-848-3792

Illinois

Illinois Department of Financial Regulation

To file a complaint directly with the Illinois Division of Financial Institutions, mail to:

Illinois Division of Financial Institutions

320 West Washington Street, 3rd Floor

Springfield, IL 62786

Toll Free Number: 1-888-473-4858

Maryland

Maryland Banking Commissioner

or complaints

Maryland residents with respect to Airbnb Payments, Inc. (License #1177237, NMLS #1177237)

500 North Calvert Street, Suite 402

Baltimore, MD 2120

Toll free number: 1-888-784-0136

New York

New York Department of Financial Services

Airbnb Payments, Inc. licensed and controlled by the New York City Department of Financial Services as a Money Transfer Company.

If after contacting Airbnb Payments, Inc.